Publications

Google Scholar Citations

Three Bishwal Books at Amazon

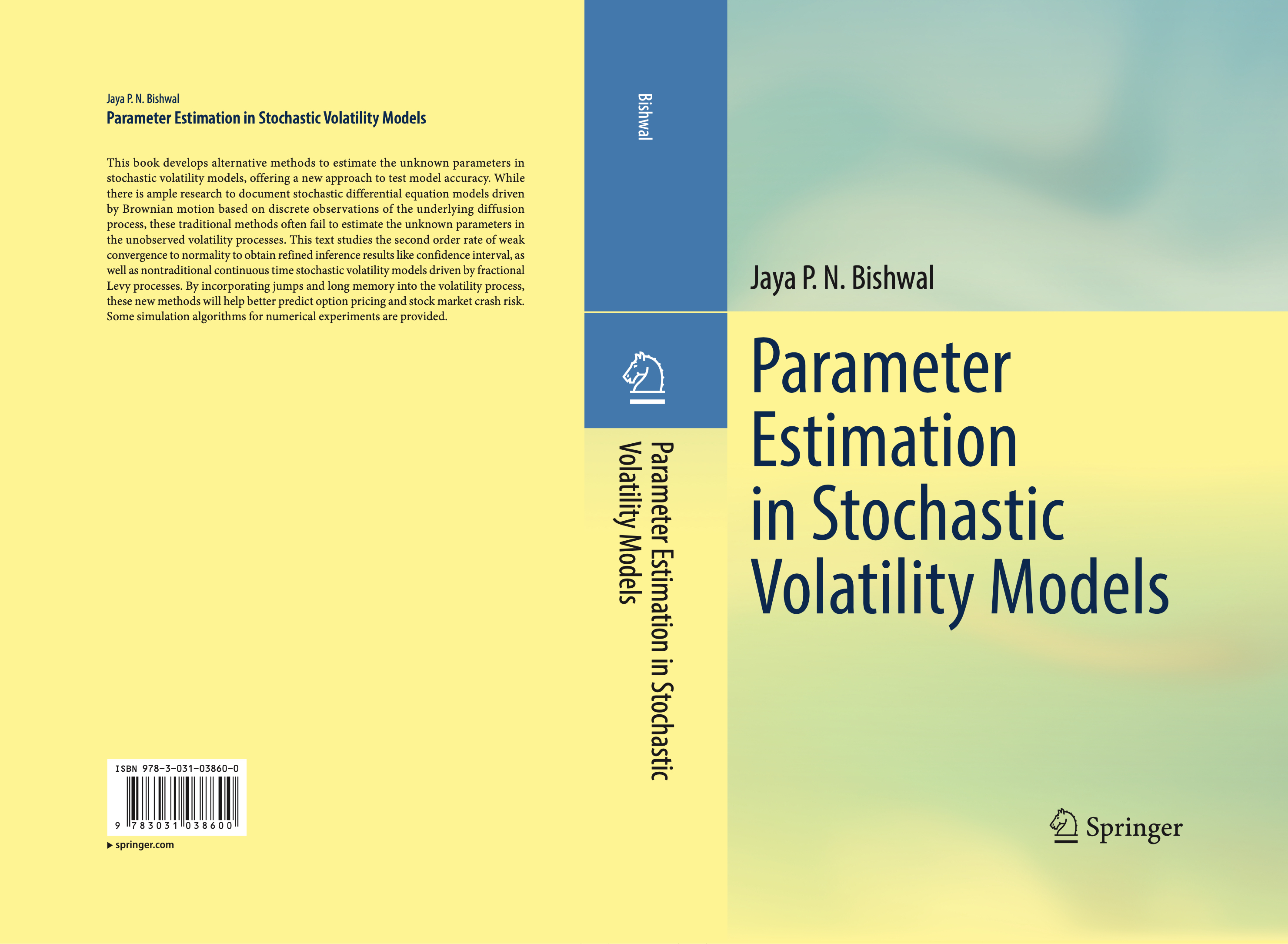

Volatility Book Picture

Total 77 Papers: 38 Papers from 2021-2025 and 56 Papers from 2011-2025

Books

|

|

3. Parameter

Estimation in Stochastic Partial Differential Equations

2. Parameter

Estimation in Stochastic Volatility Models

Springer Nature: Cham, Switzerland (2026) 366 Pages

ISBN: 978-3-031-03861-7

Springer International Publishing

Amazon

Barnes&Noble

Books-A-Million

Blackwell's

Kinokuniya

Kobo

Book Topia

Browns Books

IBS

WorldCat

|

1. Parameter

Estimation in Stochastic |

|

|

Papers/Articles

78. Third order minimum contrast estimation for nonlinear diffusions,

Journal of Risk and Financial Studies

(2026).

77. Malliavin calculus and bootstrap methods for stochastic volatility models,

European Journal of Mathematics and Applications

5 (19) (2025), 1-32.

76. Analysis of the fractional Cox-Ingersoll-Ross model based on optimal

stopping rules,

European Journal of Mathematics and Applications

5 (11) (2025), 1-25.

75. Minimum contrast estimation in fractional Ornstein-Uhlenbeck driven by

fractional Ornstein-Uhlenbeck process,

Asian Journal of Statistics and Applications 2 (1) (2025), 50-72.

74. On Poisson sampling for estimation in sub-fractional Levy stochastic

volatility models,

European Journal of Statistics

5 (4) (2025), 1-15.

73. Bootstrap confidence interval for fractional diffusions and American options,

European Journal of Mathematics and Applications 5 (5) (2025), 1-14.

72. Second order asymptotics for Vasicek model

driven by Levy processes,

European Journal of Mathematics and Applications 5 (2) (2025), 1-18.

71. Parameter estimation in Levy driven stochastic volatility models,

Journal of Econometrics and Statistics 5 (1) (2025), 57-80.

70. Nonparametric estimation in Heath-Jarrow-Morton term structure models

driven by fractional Levy processes,

Asian European Journal of Probability and Statistics 1 (2) (2024), 89-106.

69. On the Kolmogorov distance for the estimators in the Cox-Ingersoll-Ross model,

European Journal of Mathematics and Applications 4 (22) (2024), 1-32.

68. Conditional least

squares estimation for fractional super Levy processes in

nonlinear SPDEs, European Journal of Mathematical Analysis 4 (12) (2024), 1-17.

67. Quasi-likelihood and quasi-Bayes estimation in noncommutative fractional

SPDEs,

European Journal of Statistics 4 (6) (2024), 1-23.

66. Second order approximate maximum likelihood estimation

for diffusions with

random effect,

Journal of

Statistics Applications & Probability Letters

11 (1) (2024), 13-19.

65. On the Kolmogorov distance for the maximum likelihood estimator in the

explosive Ornstein-Uhlenbeck process,

European Journal of Mathematical Analysis 3 (25) (2023), 1-17.

64. On the sieve estimator for fractional SPDEs from discrete observations,

Markov Processes and Related Fields 29 (3) (2023), 367-402.

63. Approximate maximum likelihood estimation in

fractional stochastic

transport equation,

European Journal of Statistics 3 (14) (2023), 1-19.

62. Model selection using Bayes factors for the Black-Karasinski models,

Asian Journal of Statistical Sciences 3 (1) (2023), 1-12.

61. Parameter estimation for subdiffusions within proteins in nanoscale

biophysics,

Journal of Statistics, Optimization and Data Science

1 (2) (2023), 49-57.

60. Approximate maximum likelihood

estimation in semilinear SPDE,

Dynamic Systems and Applications 32 (1) (2023), 165-188.

59. Bernstein-von Mises theorem and Bayes estimation in interacting particle

systems of diffusions,

European Journal of Statistics 3 (11) (2023), 1-11.

58. Rate of convergence in the Kolmogorov distance for the minimum contrast 57. Asymptotic equivalence of discretely observed

fractional Randleman-Bartter 56. Interest rate derivatives for the fractional Cox-Ingersoll-Ross model,

55. On the Kolmogorov distance for the least squares

estimator in the fractional

estimator in the Heston model,

European Journal of Mathematics and

Applications 3 (22) (2023), 1-26.

model to a fractional Gaussian

shift,

Journal of

Statistics Applications & Probability Letters 10 (3) (2023), 173-189.

Algorithmic Finance 10 (2) (2023), 53-66.

Ornstein-Uhlenbeck process,

European Journal of Mathematical Analysis

3 (14) (2023), 1-17.

54. Quantile estimation in fractional Levy Ornstein-Uhlenbeck processes,

Model Assisted Statistics and Applications 18 (4) (2023), 279-293.

53. Bernstein-von Mises theorem for fractional SPDEs with small volatility,

European Journal of Mathematics and Applications 3 (2) (2023), 1-16.

52. Hypotheses testing in nonergodic fractional Ornstein-Uhlenbeck models,

European Journal of Statistics 3 (6) (2023), 1-15.

51. Le Cam-Stratonovich-Boole theory for Ito diffusions,

Random Operators and Stochastic Equations 31 (2) (2023), 153-176.

50. Parameter estimation for SPDEs driven by cylindrical stable processes,

European Journal of Mathematical Analysis 3 (1) (2023), 1-25.

49. MLE evolution equation for fractional diffusions

and Berry-Esseen

inequality of stochastic gradient descent algorithm for American option,

European Journal of Statistics 2 (13) (2022), 1-31.

48. Mixingale estimation function for mixed fractional SPDEs

with random effect

and random sampling,

European Journal of Mathematics and Applications

2 (12) (2022), 1-16.

47. Quasi-likelihood estimation in fractional Levy

SPDEs from Poisson

sampling,

European Journal of Mathematical Analysis 2 (15) (2022), 1-14.

46. Berry-Esseen inequalities for the fractional

Black-Karasinski model of

term structure of interest rates,

Monte Carlo Methods and Applications

28 (2) (2022), 111-124.

45. On the Stratonovich estimator for the Ito diffusion,

European Journal of Mathematical Analysis 2 (7) (2022), 1-13.

44. Berry-Esseen bounds of the quasi maximum

likelihood estimators

for the discretely observed diffusions,

Applied Math 2 (1) (2022), 39-53.

43. Mixingale estimation function for SPDEs with random sampling,

European Journal of Statistics 2 (1) (2022), 1-13.

42. Berry-Esseen bounds of approximate

Bayes estimators for the discretely observed

Ornstein-Uhlenbeck process,

Asian Journal of Statistical Sciences 1 (2) (2021), 83-122.

41. Statistics of SPDEs: From linear to nonlinear,

European Journal of Statistics

1 (1) (2021), 1-57.

40. A new algorithm for approximate maximum likelihood estimation

in sub-fractional

Chan-Karolyi-Longstaff-Sanders model,

Asian Journal of Probability and Statistics

13 (3) (2021), 62-88.

39. Bernstein-von Mises theorem and small noise asymptotics

of Bayes estimators for

parabolic stochastic partial differential equations,

Theory of Stochastic Processes

23 (1) (2018), 6-17.

38. Sequential maximum likelihood estimation in nonlinear non-Markov diffusion type

processes,

Dynamic Systems and Applications 27 (1) (2018), 107-124.

37. Robust estimation in Gompertz diffusion model of tumor growth,

Open Access Biostatistics and Bioinformatics 1 (5) (2018), 1-5.

36. Conditional least squares estimation for discretely sampled nonergodic diffusions,

Asian Research Journal of Mathematics 7 (4) (2017), 1-18.

35. Maximum likelihood estimation in nonlinear fractional stochastic volatility model,

Asian Research Journal of Mathematics 6 (2) (2017), 1-11.

34. Valuation of real options under persistent shocks,

Journal of Statistics and Management

Systems 20 (5) (2017), 801-815.

33. Hypothesis testing for fractional stochastic partial differential equations with applications

to neurophysiology and finance,

Asian Research Journal of Mathematics 4 (1) (2017), 1-24.

32. Sequential maximum likelihood estimation for reflected

Ornstein-Uhlenbeck processes

(with Chihoon Lee and Myung Lee),

Journal of Statistical Planning and Inference

142 (5) (2012), 1234-1242.

31. Stochastic moment problem and hedging of generalized Black-Scholes options,

Applied Numerical Mathematics 61 (12) (2011), 1271-1280.

30. Minimum contrast estimation in fractional Ornstein-Uhlenbeck process:

continuous and

discrete sampling,

Fractional Calculus and Applied Analysis 14 (3) (2011), 375-410.

29. Berry-Esseen inequalities for discretely observed Ornstein-Uhlenbeck-Gamma process,

Markov Processes and Related Fields 17 (1) (2011), 119-150.

28. Maximum quasi-likelihood estimation in fractional Levy stochastic volatility model,

Journal of Mathematical Finance 1 (3) (2011), 58-62.

27. Sufficiency and Rao-Blackwellization of Vasicek model,

Theory of Stochastic Processes

17 (33) (1) (2011), 12-15.

26. Financial extremes: a short review,

Advances and Applications in Statistics 25 (1) (2011), 1-14.

25. Some new estimators of integrated volatility,

Open Journal of Statistics 1 (2) (2011), 74-80.

24. Sieve estimator for fractional stochastic partial differential equations,

Annals of Constantin

Brancusi 5 (1) (2011), 9-18.

23. Estimation in interacting diffusions: continuous and discrete sampling,

Applied Mathematics

2 (9) (2011), 1154-1158.

22. Milstein approximation of posterior density for diffusions,

International Journal of Pure and

Applied Mathematics 68 (4) (2011), 403-414.

21. Maximum likelihood estimation in Skrorohod stochastic differential equations,

Proceedings of the American Mathematical Society

138 (4) (2010), 1471-1478.

20. Uniform rate of weak convergence

of the minimum contrast estimator in the

Ornstein-Uhlenbeck process, Methodology and Computing in Applied Probability

12 (3) (2010), 323-334.

19. Conditional least squares estimation in diffusion processes based on Poisson sampling,

Journal of Applied Probability and Statistics 5 (2) (2010), 169-180.

18. Sequential Monte Carlo methods for stochastic volatility models: a review,

Journal of Interdisciplinary Mathematics 13 (6) (2010), 619-635.

17. M-estimation for discretely sampled diffusions,

Theory of Stochastic Processes

15 (31) (2) (2009), 62-83.

16. Berry-Esseen inequalities for discretely observed diffusions,

Monte Carlo Methods and

Applications 15

(3) (2009), 229-239.

15. Large deviations in testing fractional Ornstein-Uhlenbeck

models, Statistics & Probability

Letters 78 (8) (2008), 953-962.

14. Large deviations and Berry-Esseen inequalities for estimators in nonlinear nonhomogeneous

diffusions,

RevStat - Statistical Journal 5 (3) (2007), 249-267.

13. A new estimating function for discretely sampled diffusions,

Random Operators and

Stochastic

Equations 15 (1) (2007), 65-88.

12. Sequential maximum likelihood estimation in semimartingales,

Journal of Statistics

and Applications 1 (2-4)

(2006), 143-153.

11. Rates of weak convergence of

approximate minimum contrast estimators for the

discretely observed

Ornstein- Uhlenbeck process,

Statistics & Probability Letters

76 (13) (2006), 1397-1409.

10. Maximum likelihood estimation in

partially observed stochastic differential system

driven by a fractional

Brownian motion,

Stochastic Analysis

and Applications

21

(5) (2003), 995-1007.

9. The Bernstein-von Mises theorem and

spectral

asymptotics of Bayes estimators for

parabolic SPDEs, Journal of the Australian

Mathematical Society 72 (2) (2002), 287-298.

8. Rates of

convergence of approximate maximum likelihood estimators in the

Ornstein-Uhlenbeck process, Computers & Mathematics with

Applications

42

(1-2) (2001), 23-38 (with Arup Bose).

7. Accuracy of normal approximation for

the maximum likelihood and the Bayes

estimators in the Ornstein-Uhlenbeck process using random normings,

Statistics & Probability Letters

52 (4) (2001), 427-439.

6. Rates of convergence of the posterior

distributions and the Bayes estimators in

the Ornstein-Uhlenbeck process,

Random Operators and Stochastic

Equations

8 (1)

(2000), 51-70.

5. Sharp

Uhlenbeck process, Sankhyā Series A 62 (1), (2000), 1-10.

4. Large deviations inequalities for the

maximum likelihood estimator and the Bayes

estimators in nonlinear stochastic

differential equations, Statistics & Probability Letters

43 (2) (1999),

207-215.

3. Bayes and sequential estimation in Hilbert

space valued stochastic differential equations,

Journal of the Korean Statistical

Society 28 (1)

(1999), 96-108.

2. Speed of convergence of the maximum

likelihood estimator in the Ornstein-Uhlenbeck

process, Calcutta Statistical Association

Bulletin 45 (1995),

245-251(with Arup Bose).

1. Approximate maximum likelihood

estimation for diffusion processes from discrete

observations,

Stochastics 52 (1995), 1-13 (with M. N.

Mishra).

Technical Report

1. A note on inference in a bivariate normal distribution model (with Edsel Pena)

SAMSI Technical Report #2009-3